FICC Focus: “Active Management, Fixed Income Chaos: Masters of the Muniverse”

August 30, 2023

Clinton Investment Management, CEO and founder Andrew Clinton joined Bloomberg Intelligence’s Eric Kazatsky and Karen Altamirano on the FICC Focus weekly podcast on fixed income, credit, currencies, and commodities. In this episode—”Active Management, Fixed Income Chaos: Masters of the Muniverse”—they discuss the muni market, expectations around recession, and general outlook post-Jackson Hole and for the fourth quarter ahead.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.

The US economy has continued to contract in Q2, according to the Atlanta Fed’s GDPNow -1.2% forecast

The US economy may already be in recession

The recent rise in tax-free muni yields has created a window of opportunity through which investors can now capture very attractive yields, which, on a taxable equivalent basis, rival the nominal, annualized returns that are often associated with much higher risk assets

A hard landing is increasingly becoming the base case for the US economy

We are recommending investors with exposure to short-term municipal bonds consider seriously moving out of what we believe are the most unattractive short-term, high-quality maturities and extend into longer duration bonds

High quality short-term munis are trading at the lowest yield-to-Treasuries ratio, 55%, that we have seen since the beginning of this year

Andrew Clinton CEO

Interest rates rose meaningfully during the second quarter, largely due to investor fears that peak inflation would persist, or worse accelerate, which would force the Federal Reserve to hike interest rates dramatically as it seeks to return inflation to its 2% target. Consistent with the expectations we shared in our Q1 Market Commentary, the economy has already begun to slow rapidly, as evidenced by the -1.6% contraction in GDP in Q1. The US economy has continued to contract in Q2, according to the Atlanta Fed’s GDPNow -1.2% forecast. This is extraordinary as the second quarter of the year has historically been one of resurgent growth. This is an ominous signal for the direction of the economy going forward in our view. Two quarters of back-to-back contraction in economic activity is consistent with the technical definition for an economic recession. Therefore, the US economy may already be in recession. Market strategists have broadly dismissed this reality, preferring to place their faith in the hope that the Fed can orchestrate a soft landing instead. This can be seen clearly in the Bloomberg survey of economists, which in May placed the odds of a US recession in the next 12 months at barely 30%. As our loyal readers may recall, Clinton Investment Management (CIM) noted the slowing economic data in Q1 and recommended investors begin preparing for recession, as we believed a material slowing in economic growth would result in the destruction of wealth through a significant devaluing of risk assets. We now know that those concerns were warranted, and our advice was well placed, as the asset classes that inflated the most, due to fiscal stimulus and quantitative easing, including crypto currencies, equites, high yield bonds, and even the broader commodity complex, have all seen significant price declines and the destruction of trillions of dollars of wealth, removing liquidity from the market, just as the Fed intended.

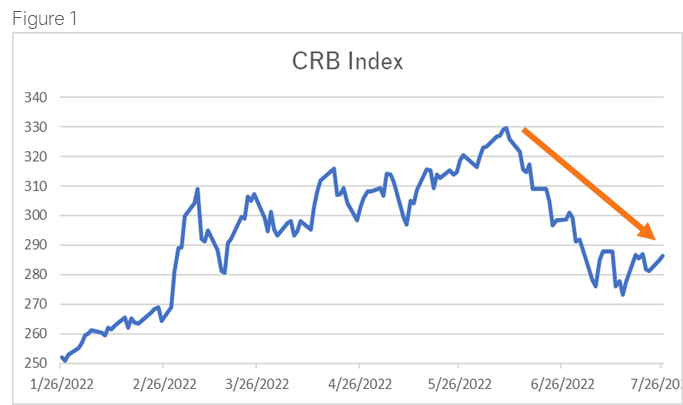

US economic data has turned decidedly negative as illustrated by the recent Pending Home Sales, -19.8% year-over-year, New Home Sales, -8.1% month-over-month, while weekly jobless claims have risen for four consecutive months and now stand at +244,000. Almost the entirety of the commodities complex has turned meaningfully lower as well. Raw materials prices are now falling, see Figure 1. This is very good news for anyone concerned about the level of inflation going forward.

It is now clear to us that the average consumer is not strong at all, contrary to what many would have us believe. These conditions, taken together, support our view that inflation has likely peaked while US and Global economic growth continues to decline, as the Fed continues to tighten financial conditions at a pace we have not seen in almost twenty years.

Source: Bloomberg

Bell-weather, multinational corporate earnings from Walmart, Amazon, Target, Best Buy, and now AT&T have deteriorated much faster than expected. AT&T’s recent earnings miss was particularly alarming as it speaks directly to the general health of the millions of consumers it serves. AT&T specifically stated that its earnings where meaningfully impaired by “delayed” payment of bills by its customers. When we consider that revolving consumer credit, in the form of credit card debt, has exploded year-to-date, the reality that consumers are now struggling to simply pay their phone bills raises serious concerns about the degree of economic pain consumers are experiencing, as well as the deterioration in their personal balance sheets they are enduring. It is now clear to us that the average consumer is not strong at all, contrary to what many would have us believe. These conditions, taken together, support our view that inflation has likely peaked while US and global economic growth continues to decline, as the Fed continues to tighten financial conditions at a pace we have not seen in almost twenty years.

The broader bond market is just now beginning to price in the probability of a recession in the near-term. Indications of this can be seen in the more than 60 basis point decline in 10-year Treasury yields, from a high of 3.40% to 2.76%, at the time of this writing. The broader market narrative has shifted dramatically from a fear of inflation to a fear the Fed will make or may have already made, the policy mistake of tightening too much, as they have in every other US expansion in history. We share this fear as it is our expectation the Fed will indeed go too far, including the 75 basis point increase in the Federal Funds rate expected this month. A hard landing is increasingly becoming the base case for the US economy. As a result, the Treasury yield curve has begun to flatten meaningfully, as yields on short-term bonds have surged higher while long-term bonds yields have fallen. This bear flattening of the curve has resulted in two-year Treasury yields now yielding more than 30-year bond yields, a conditioned referred to as an inverted yield curve. The inverted curve slope of the entire curve is extremely important as it has been an excellent predictor of recession over the course history, with roughly 90% accuracy.

Given that the Fed has just begun raising “short-term” interest rates, and unwinding its tremendous balance sheet, via Quantitative Tightening (QT), we believe the curve could become deeply inverted in the not-too-distant future. QT is the Fed policy that results in the Fed allowing what is expected to be over $90 billion a month in marketable securities it holds on its balance sheet to mature without reinvestment of the proceeds. Given that the US Treasury will be forced to issue new Treasury bonds to fund the US’s ever growing debt obligations, investors and banks will be forced to buy those securities the Fed would have purchased otherwise, thereby removing additional liquidity from the market, resulting in a further crowding out of investment in risk assets more broadly in our view.

While municipal bond yields have largely moved up in sympathy with Treasury bond yields over the past six months, munis continue to clearly demonstrate their wealth preservation qualities as the asset class remains, not only the best performing, fixed income asset class on a relative return basis, but they have also outperformed domestic and global equity markets as the value of municipal bonds have declined by a smaller degree. It is worth noting, that the recent rise in tax-free muni yields has created a window of opportunity through which investors can now capture very attractive yields, which, on a taxable equivalent basis rival the nominal, annualized returns that are often associated with much higher risk assets.

Credit quality in the municipal bond market remains the strongest it has been in over two decades due to an unexpected flood of higher tax collections, together with over $500 billion in stimulus money that was delivered to state and local governments, schools, and hospitals via the American Rescue Plan in 2021. As the economy slows and interest rates decline further, municipal bond investors are likely to benefit from the lower risk and higher tax-free cash flow munis provide, while enjoying the potential for principal appreciation associated with falling interest rates and the flattening of the muni curve.

Source: Bloomberg

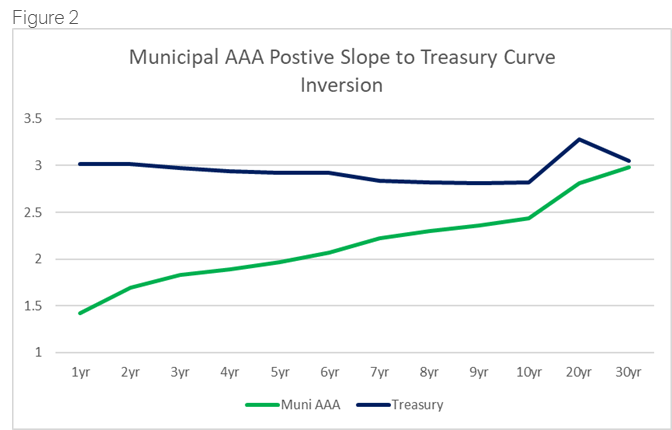

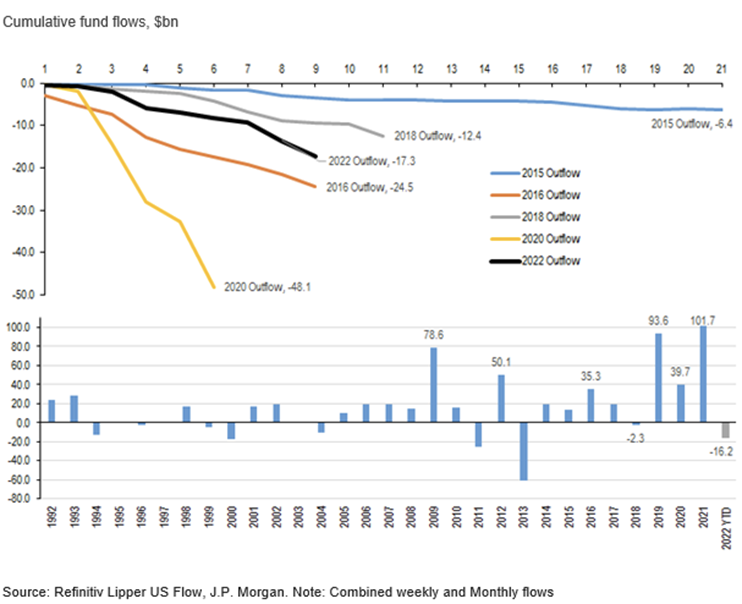

As we discussed recently, the current slope of the Treasury yield curve is inverted -8 basis points between two year and thirty-year Treasury bonds (2s/30S). What is fascinating is that this condition does not exist in the municipal bond market. The 2s/30s slope in the muni market is actually +129 basis points, see Figure 2. This positive slope provides additional yield incentive to investors to extend out the curve as the muni market is structurally mispriced relative to Treasuries. This dislocation and inefficiency between munis and Treasuries occurs on rare occasions, largely due to retail investor outflows from mutual funds, as has been the case year-to-date. A record +$80 billion has flowed out of the municipal bond mutual funds year-to-date as panicked retail investors sell first and ask questions later, leaving extraordinary value in their wake, in our view.

This positive slope provides additional yield incentive to investors to extend out the curve as the muni market is structurally mispriced relative to Treasuries. This dislocation and inefficiency between munis and Treasuries occurs on rare occasions, largely due to retail investor outflows from mutual funds, as has been the case year-to-date.

We believe these investors are not sufficiently heeding the important economic signal the long-end of the Treasury market is sending. As a result, we are recommending investors with exposure to short-term municipal bonds consider seriously moving out of what we believe are the most unattractive short-term, high quality maturities and extend into longer duration bonds. We believe the long end of the muni market does not accurately reflect slowing growth prospects and the probability of lower interest rates going forward. The opportunity costs of staying in short maturities in our view is, therefore, quite high. High quality short-term munis are trading at the lowest yield-to-Treasuries ratio, 55%, that we have seen since the beginning of this year, when ratios were at record lows. On the contrary, ratios of long-term munis are over now 100%, which implies the tax-exemption of munis is largely worthless. This presents a rare opportunity for almost anyone, in any tax bracket, to benefit from the attractive value that long-term munis now offer, especially given our expectation that materially higher interest rates are unlikely going forward. Lastly, the recent rise in short-term bond yields has generated capital losses for investors that can be harvested with the goal of modestly extending duration to pick up higher tax-free yields and higher total return over time.

The impact of Fed action, now and in the future, cannot be overstated. Therefore, we are encouraging investors to prepare for the high likelihood of recession by increasing their exposure to assets that carry less risk, including cash, high quality longer duration fixed income, and municipal bonds in particular. Given the very attractive yields on a tax-free and taxable equivalent basis that munis provide, we believe clients are being well compensated as they await the deepening of the recession and a corresponding decline in interest rates.

Clinton Investment Management News

We are excited to share there our strategies were recently launched on the Morgan Stanley platform and are now available to over 16,000 Morgan Stanley advisors and their clients. We would also like to invite you to visit us at our new website www.clintoninvestment.com to view additional content about our firm and our strategies.

Please do not hesitate to contact us with any questions regarding this piece or the current market opportunity we are now seeing.

Best Regards,

Andrew Clinton

CEO

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product,madereference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals.Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for reviewupon request.

Municipal bonds are now two standard deviations cheap to historical fair value, when looking at the relationship of tax-free yields relative to Treasuries.

Investors can now achieve tax-free yields that are higher than the nominal yields of taxable bonds.

Municipal bond ratios are above 100% of Treasury yields.

Investors at almost every tax bracket now benefit from owning municipal bonds, a rare condition that we do not believe will persist.

Absolute yields now available on our municipal bonds strategies translate to 6.75% to 8.00% on a taxable equivalent basis.

Andrew Clinton CEO

Winter is coming, both figuratively and literally, for global economies and corporations. Consistent with the outlook we shared in our most recent market commentary, the US economy is beginning to slow rapidly. The clearest illustration of this can be seen in the -1.4% Q1 GDP growth, however, we are now seeing multinational, bellwether companies, including Walmart, Amazon, Target, Ross Stores, Best Buy, and Snap, to name a few, reporting extremely disappointing earnings, guiding down their outlook for future profits, and experiencing breathtaking declines in their share prices. We believe the disappointing earnings announcements are highly correlated with the general health of the US consumer. Given that household consumption represents almost 70% of US GDP, this is a very concerning trend. The US economy is facing a perfect storm of elevated inflation, tightening financial conditions, and a materially weakened consumer. In the case of Walmart, when seeking to explain its disappointing earnings, the company referenced being “overemployed” as well. That is the condition that exists when companies have too many employees and insufficient sales to support them, negatively impacting corporate profitability. This often leads to significant layoffs and rising unemployment over time. Walmart is one of the largest employers in the world, with a total of 2.3 million associates, 1.6 million in the US alone. It’s statement is an ominous sign for broader unemployment levels going forward. Declines in earnings and lowered profit guidance of this scale are causing a dramatic shift in investor sentiment. Given that we raised our concerns regarding the growth risks facing the US economy some time ago, we thought timing was appropriate to provide an update on our outlook as we are now meaningfully more constructive on the direction of interest rates and tax-free municipal bonds in particular.

A frightening decline in risk asset valuations is happening at time when tax-free yields for municipal bonds are the highest they have been since the depths of the pandemic and the Great Financial Crisis. Yet, underlying municipal credit quality is the strongest it has been in over three decades in our view. Twenty consecutive weeks of municipal bond fund outflows, from retail investors, has exerted temporary, upward pressure on municipal bond yields, causing the performance of municipal bonds to remain constrained, even as Treasury yields are falling. This has created a market condition whereby municipal bonds are now two standard deviations cheap to historical fair value, when looking at the relationship of tax-free yields relative to Treasuries. Investors can now achieve tax-free yields that are higher than the nominal yields of taxable bonds. When municipal bond ratios are above 100% of Treasury yields, as they are now, this condition has historically represented an excellent entry point for investors as this relationship implies there is little to no value in the taxexemption of municipal bonds. Yet, investors at almost every tax bracket now benefit from owning municipal bonds, a rare condition that we do not believe will persist. As our clients and advisors are aware, during the first four months of the year, we were cautious in committing new cash to the municipal bond market, given the unrelenting rise in rates. We have pivoted meaningfully, over the last few weeks, as recent economic data support our view that inflation and the US economy are beginning to slow meaningfully. As a result, we are much more constructive on the outlook for fixed income more broadly and municipal bonds in particular. Absolute yields now available on our municipal bonds strategies translate to 6.75% to 8.00% on a taxable equivalent basis, for those in the highest tax bracket. While these yields are dependent on market conditions and can change quickly, we believe the current level of yields are extremely compelling, offering investors substantial compensation for the very low default risk associated with municipal bonds. Considering the low expected returns for risk assets over the next five to ten years, we believe municipal bonds will continue to provide safety and compelling returns over that period.

As we look out over the remainder of the year and into 2023, economic uncertainty is clearly rising while economic growth is materially slowing. The Fed has only just begun raising rates and is set to begin reducing its balance sheet next month through quantitative tightening. Asia and Europe are slowing, and multinational corporations are feeling the pain of the weakened consumer, as evidenced by the recent alarming earnings announcements and corresponding share price declines. Wealth destruction of this nature is going to have significant impact on consumer demand and that is by the Fed’s design. We see no reason why this trend will not continue until the economy is in recession or the Fed pauses whichever comesfirst. Given that CPI is a backward-looking indicator, we believe a recession will likely arrive first as the Fed has never reduced inflation by more than 2.9% without causing a recession. As such, we believe the time has come for investors to prepare for the eventuality of a US recession. With that in mind, investors should begin to materially add to their municipal bond allocations. Municipal bonds are an extremely safe store of value and perform quite well during periods of economic deceleration. Investors with high allocations to cash yielding close to 0%, or risk allocations which need to be modified for the new economic reality, will benefit from the attractive tax-free municipal bonds now offer.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product,madereference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals.Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for reviewupon request.

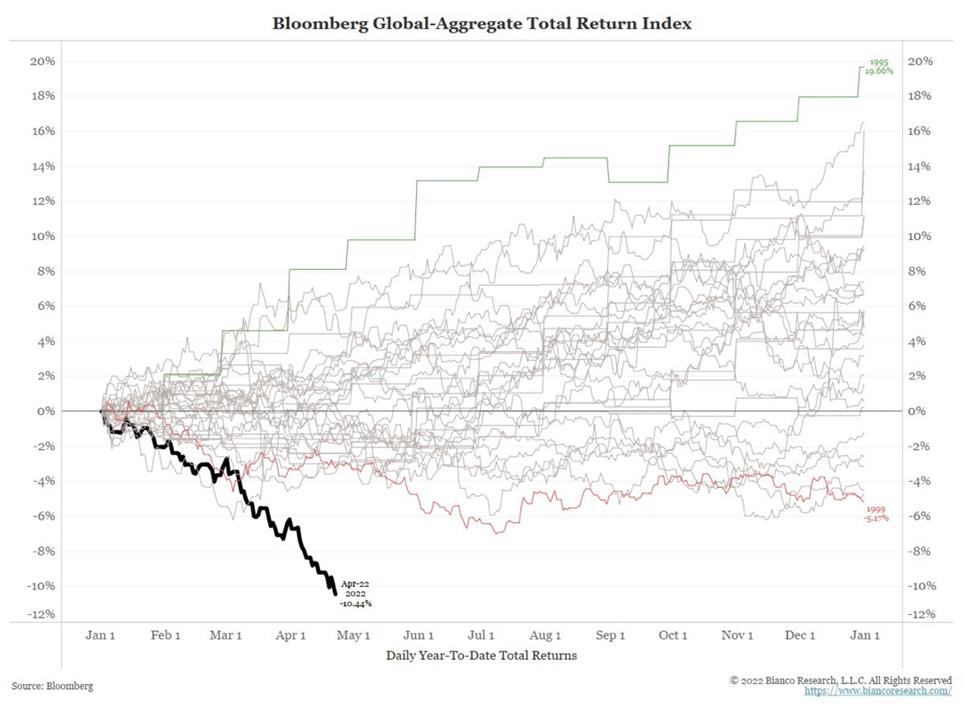

Fixed income markets have experienced the worst start to a year, from a performance perspective, in forty years.

Municipal bonds are now two to three standard deviations cheap relative to taxable bonds.

Moody’s issued 817 upgrades for municipalities in 2021 compared to 307 down grades.

Since 1927, the Fed has never reduced inflation by more than 2.9% without causing a recession.

Andrew Clinton CEO

The first four months of 2022 have been the most tumultuous period for investors since the onset of the pandemic in March of 2020. For fixed income markets, it has been the worst start to a year, from a performance perspective, in forty years, see Figure below. Elevated inflationary pressures, resulting from extended COVID lockdowns and corresponding supply chain dislocations, together with tremendous fiscal stimulus, have taken center stage in terms of their contribution to inflation. The outbreak of war in Ukraine has further amplified pressure on energy and commodities prices. The Fed pivoted dramatically, in Q4 2021 from a position on the economy of watchful patience and a belief that inflation would prove transient, to its now, much more, hawkish view on inflation. The Fed is stridently messaging to markets its intent to forcefully use interest rate hikes to break the back of inflation. This shift in narrative has surprised markets and contributed to a dramatic rise in volatility and uncertainty, raising recession risks meaningfully. The impact of tightening financial conditions can be seen in the recent -1.4% contraction in Q1 US GDP growth. Some, in the investment community, have attributed this contraction to a one-off aberration, resulting from a surge in imports. We believe dismissing this important economic indicator is the equivalent of whistling past the graveyard.

While we see the surge in imports as an important indication that the supply chains are healing, a resulting surge in inventories is occurring at a moment when the economy and consumer spending is likely to slow materially. We firmly believe the trajectory of US economic growth is decidedly downward and should not be dismissed. As domestic economic growth continues to slow, we expect the slowdown in growth globally to further weigh on economic activity domestically. Stagflationary forces, including higher fuel prices and a corresponding reduction in spending and slowing growth have already begun to change consumer behavior and spending decisions, as can be seen in the 8% decline in real, inflation-adjusted, gasoline consumption in March. Consumers are clearly choosing to drive less due to high gas prices. If high gasoline prices persist, and we expect they will, it will likely further dampen economic activity more broadly. We also expect a further reduction in discretionary spending as the Fed tightens financial conditions. The equity market has begun to price in this new reality, as evidenced by the recent performance of many procyclical sectors within the S&P 500. Asset Management, Rails, Construction Materials, Media and Entertainment, Homebuilders, Home Furnishings, Retailing, Banks, and Consumer Electronics sectors are all down 28%, 13%, 19%, 31%, 40%, 20%, and 23% respectively year-to-date, while the Industrial Materials and Electrical Equipment sectors are down 20% and 18% respectively. Software is down 25% while telecom equipment is off by 19%. The equity market declines support the view that the Fed will be successful in destroying demand, together with wealth, resulting in lower inflation over time. Mortgage applications are now lower by over 50%, year-over-year, while refinancing activity has fallen by roughly 70% over the same period. This will have a material impact on housing price affordability and ultimately exert downward pressure on housing prices and sales volume. The probability of a Fed policy mistake has risen considerably. Bond Markets have now priced-in over 200 basis points of rate hikes, yet the Fed has only raised rates by 0.25% in March and 0.50% yesterday. We believe the Fed will ultimately tighten financial conditions too much, pushing the economy into a recession, as it has in almost every instance over the course of history. Since 1927, the Fed has never reduced inflation by more than 2.9% without causing a recession, according to Guggenheim research. It is also worth noting that the last time the Fed hiked rates into a slowing economy was 2018. The impact of the Fed actions resulted in a crash in equity markets in December of that year. The Fed was forced to rapidly reverse course soon thereafter. We believe the outcome will be similar in this instance, assuming the Fed implements the rate hikes the market is now expecting.

The municipal bond market has not been immune to the rise in interest rates year-to-date. Municipal bonds have endured the worst start to the year, in terms of performance, in recorded history. Municipal bond prices have declined across the entire maturity spectrum. The 5 year, 7 year, 10 year and 30 year, Bloomberg Barclays Municipal Bond indices, returned -5.10%, -5.70%, -6.23% and -8.65% respectively in Q1. It came as a painful surprise to more passive investors that high quality, short maturity bonds did not provide the protection they expected. As unsettling and unwelcome as this experience has been for municipal bond investors, moments such as these provide a lens through which we can focus on the primacy of deep underlying credit research. Identifying issuers with solid underlying fundamentals can provide investors with the confidence that is needed to ride out temporary periods of rising rates. The decline in municipal bond prices has been exacerbated by sixteen consecutive weeks of outflows from municipal bond mutual funds. The over $40 billion in outflows from bond funds has resulted in a temporary decline in market liquidity to due forced selling by mutual fund managers, causing yields to rise and spreads to widen. The current outflow cycle is now the fourth longest outflow cycle in the history of the municipal bond market and has caused municipal bonds to cheapen relative to other fixed income alternatives. Municipal bonds now offer tax-free yields that are the same or higher than taxable bonds. Stating it another way, municipal bonds are now two to three standard deviations cheap, relative to taxable bonds. We do not expect this relationship to be sustained. Nontaxable, crossover buyers are already finding the absolute level of municipal bond yields to be compelling and have begun buying, even though they may not fully benefit from their tax-exemption.

Investors can be comforted by the knowledge that the US economy is very late in the current business cycle. The Fed has already begun the tightening cycle and we believe it will not stop until it pushes the economy into recession. We also know that, during recessions, interest rates fall dramatically, thereby, restoring principal value that was lost due to price reductions that occurred when rates where rising. It is important to note that investors with a long-term, investment horizons who have additional liquidity to take advantage of the currently very attractive level tax-free yields, should do so in our view. Valuation is now a major source of support for the municipal bond market going forward.

Some good news in this environment is that the outlook for municipal credit quality continues to be the brightest it has been in over two decades. The combined benefits of over $500 billion in fiscal support, provided to municipalities from the American Rescue Plan, together with dramatically higher tax collections municipalities have enjoyed since the onset of the pandemic, have materially strengthened underlying municipal credit quality on a broad scale. Moody’s issued 817 upgrades for municipalities in 2021 compared to 307 down grades. Through February 2022, municipal bond defaults totaled just $360 million, or 0.10% of the over $4 trillion of municipal bonds outstanding. Despite the stable to improving credit outlook, lower investment grade, Baa/BBB rated bonds, have widen by over 50 basis points, reflecting the weaker demand environment created by mutual fund outflows. Given the inefficiencies this outflow cycle has created, we continue to believe the best opportunities exist in lower investment grade bonds, given that investors enjoy very attractive compensation in the form of higher yields, together with low credit risk. The 4% to 4.25% tax-free yields investors can now achieve in lower investment grade municipal bonds equate to over 7.2% on a taxable equivalent basis, for those in the highest tax-bracket. We believe these yields are extremely compelling when one considers that the expected return on risk asset allocations may be as low as 3% to 5% annually over the next 10 years, according to Vanguard.

As we look forward to the coming weeks and months, we fully expect the uncertainty and volatility that has plagued markets to persist, however it may also increase as tightening financial conditions exert further downward pressure on risk asset valuations. In the coming days we will also learn if the US economy has reached peak inflation, which is our base case. As such, we believe the Fed’s intentions of using interest rate hikes to destroy demand for goods and services will be successful. They have all the tools necessary to break the back of inflation. The challenge the Fed is faced with is the growing risk that their actions will push the US economy into recession sooner rather than later. The Q1 GDP contraction is the best illustration of the precarious path the Fed is now on. Slowing growth has clearly arrived at the same time that stagflationary forces are pushing the prices of everyday items, such as food, energy, and the cost of housing to unsustainable levels. Something is going to break. When it does, the US economy will be the lesser for it.

If you should have any questions regarding this commentary or the municipal bond market more broadly, please do not hesitate to contact us directly.

Best Regards, Andrew Clinton CEO

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product,madereference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals.Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for reviewupon request.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product,madereference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals.Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for reviewupon request.

Given recent municipal bond market volatility, we thought it would be helpful to provide historical context and perspective through the lens of prior periods of interest rate fluctuations. We’ve drawn parallels to the most recent episode as we are reminded of the prescient Mark Twain observation that “history does not repeat itself, but it often rhymes.”

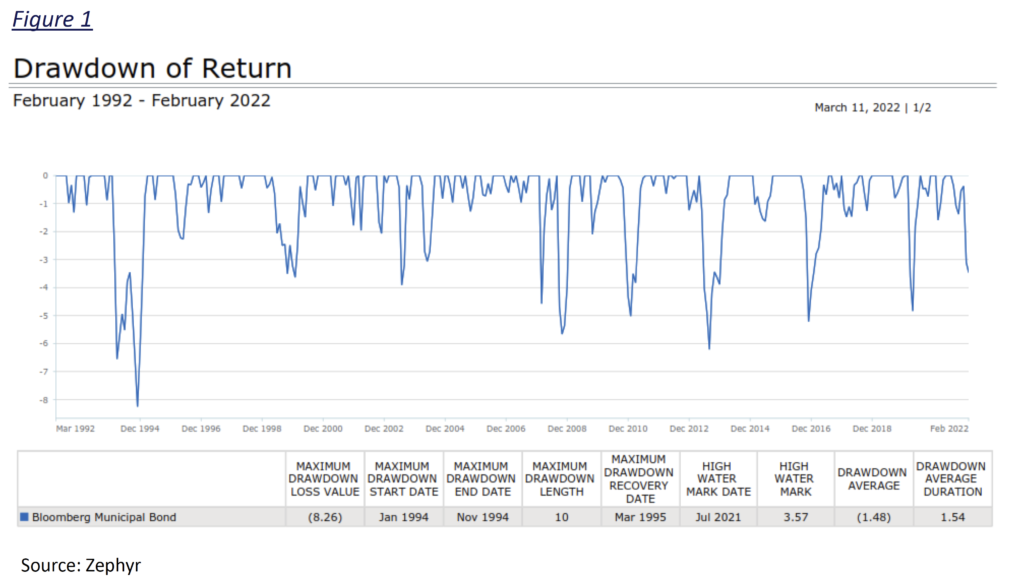

For investors new to municipal bond investing, it is important to note that periods of rising municipal bond yields are quite common and should be expected. As you can see in Figure 1 below, over the last thirty years, there have been numerous instances of rising municipal bond yields, thirteen of which resulted in drawdowns of greater than -2.00%.

Through the analysis of this data, one can see that episodes of rising municipal bond yields and corresponding bond price drawdowns are both temporary and self-correcting. While the corresponding drawdown in principal value associated with these periods of rising yields may be unwelcome and concerning for investors, we are reminded that rate fluctuations are a natural condition associated with periods of economic and geopolitical uncertainty. This moment is no different. As students of the market, we draw confidence from the knowledge that business cycles have clearly defined beginnings, known as expansions, followed by economic contractions, known as recessions. We also know that, over the course of history, recessions have been caused by one of three powerful economic forces including wars, inflation, and Federal Reserve interest rate tightening cycles. What makes this moment truly extraordinary is the harsh reality that the US economy is faced with all three of these forces at the same time. These negative economic impulses are expected to accelerate the end of the current expansion, bringing forward recession. The knowledge, that a recession is forthcoming, should provide confidence to bond holders who may be concerned by the recent move higher in rates, as interest rates are expected to fall as growth slows and the current expansion ends.

While headlines and news may understandably be alarming, it is important to note that we have experienced similar episodes of this nature over time. Periods of uncertainty can create anxiety for us all. However, it is in these moments of uncertainty that we must refocus our minds on the fundamental principles of successful investing, while doing our best to control our emotions. We often remind our clients that one of the most important principles of successful investing is to remain calm and firmly committed to one’s long-term investment horizon and goals. For example, we encourage the investors we serve to maintain investment horizons that are consistent with a full business cycle. This commitment enables investors to see past current market volatility, in order to enjoy the benefits of the recovery in bond prices that are associated with eventual recessions. The essentiality of an investor’s commitment to this central tenet cannot be overstated, as it provides investors with confidence and comfort in their knowledge that rates will decline once this expansion ends, in the not-so-distant future.

While a deep knowledge of economic forces and market history are vital for sophisticated investors to achieve success in the municipal bond market, it is also critical to understand the tendencies of investors who may not have the same access to this knowledge or have the same benefit of experience. Free markets enable investors to make decisions for a host of reasons which, unfortunately, may be inconsistent with an investor’s best interests. An illustration of this can be seen in the nine consecutive weeks of municipal bond fund outflows we have seen year-to-date. This outflow cycle has been the primary cause of the recent rise in municipal bond yields and the corresponding decline in prices. Treasury bond yields began rising in January dragging the yields of municipal bonds higher. The common reaction of retail investors in municipal bond funds is to sell their mutual fund holdings at the first indication of a negative return on a fund’s Net Asset Value. This overreaction triggered cascading redemptions of open-end and exchange traded municipal bond funds. These redemptions have resulted in forced selling by fund managers into a municipal bond market that has thus far been disinclined to step forward to bid on securities, given that broker dealers have substantially reduced their committing capacity for municipal bond trading, over the past twenty years. From our Econ 101 classes we know that a greater supply of bonds for sale with diminished demand for those bonds, results in lower prices, at least until those bids, has persisted resulting in negative returns for municipal bond investors year-to-date. The current outflow cycle is now among the longest in the history of the municipal bond market.

It is important to note that the dual windfalls of dramatic revenue increases, resulting from unexpectedly high municipal tax collections, together with the over half a trillion dollars in fiscal support delivered to municipalities by the American Rescue Plan, have delivered the strongest outlook for municipal credit quality in decades. It is also important to remember that during prior periods of rising interest rates, the majority of the broader rate increase has occurred prior to the first Fed rate hike. We firmly believe that this moment presents an attractive entry point for investors, given the Fed’s plans to start hiking rates this week. We are, therefore, encouraging investors to revisit their investment goals and horizons to determine if they can take advantage of this unique window of opportunity.

If you should have any questions regarding this commentary or the municipal bond market more broadly, please feel to reach out to us directly.

Sincerely, Andrew Clinton CEO

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.