- Given the breathtaking drawdown in US equity markets, and fixed income yield and price volatility, we believe the term that best captures the current market tone is shaken.

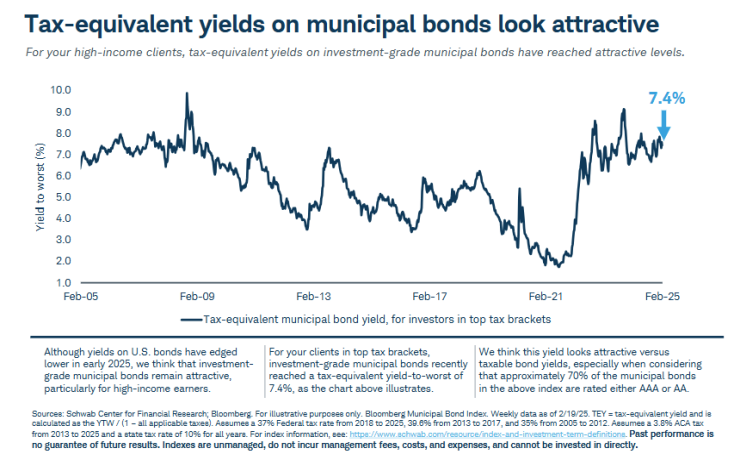

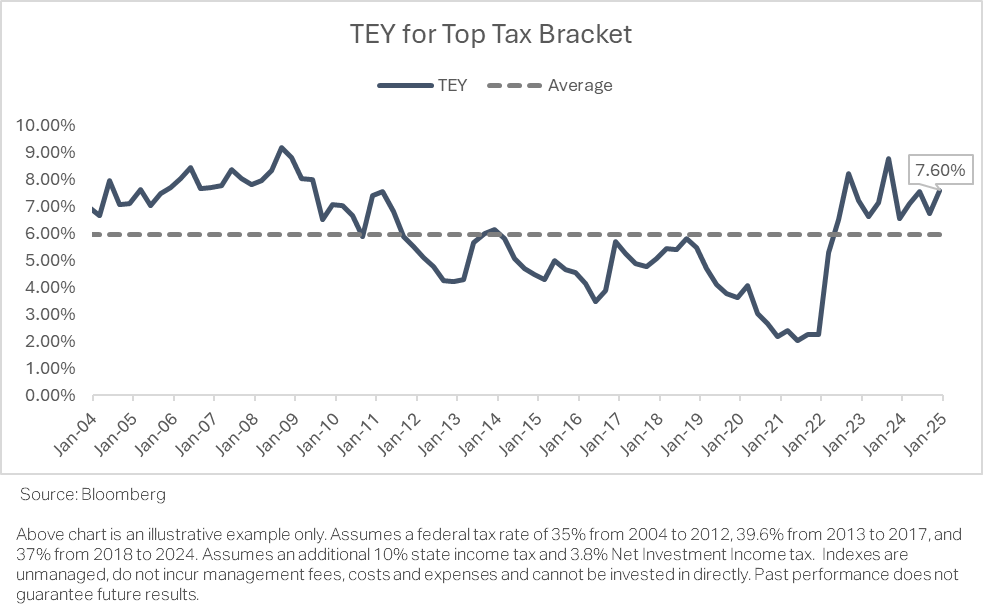

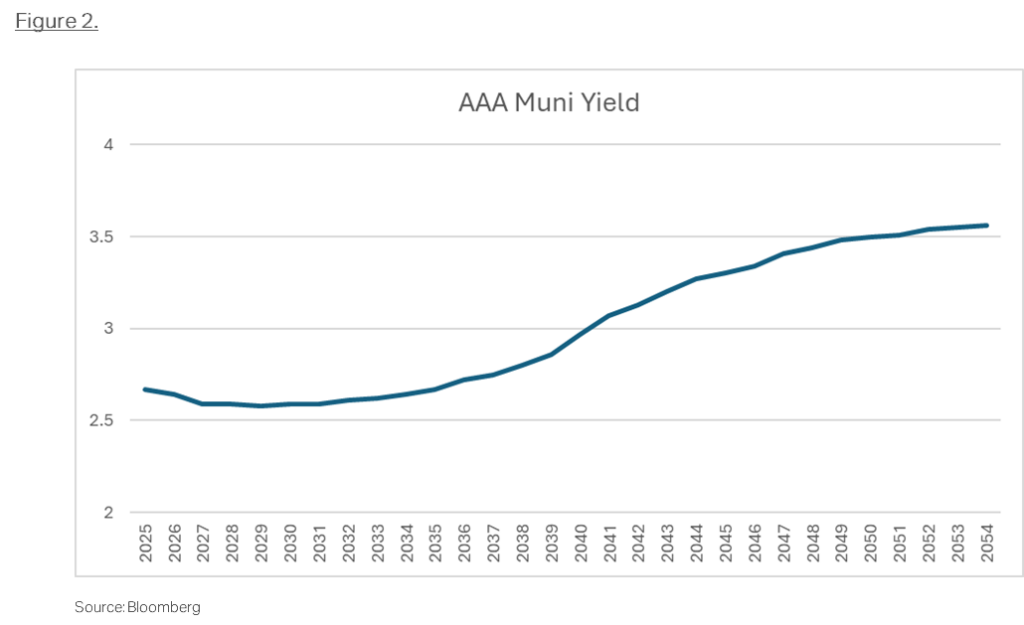

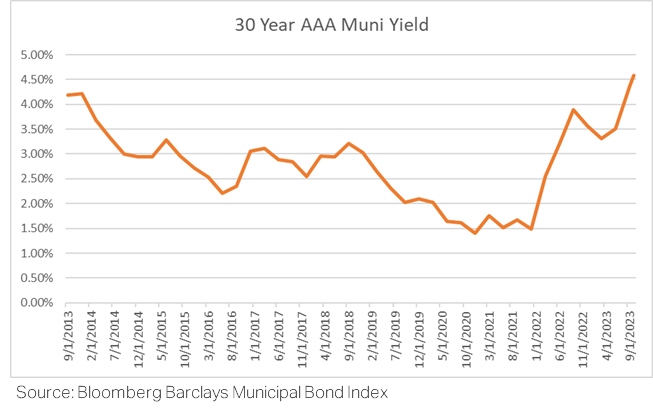

- The absolute level of tax-free munis in the 20-30 year area of the curve is now approaching 5.00%, or a taxable equivalent yield of almost 10.00%.

- Retroactively removing the tax-exemption of munis would likely violate the Federalist underpinnings of the 10th Amendment.

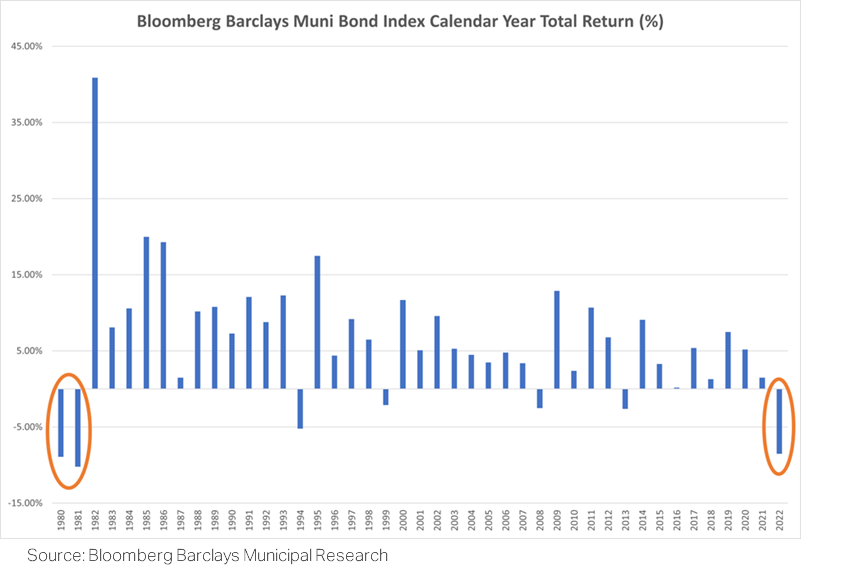

- While it is often difficult in times of uncertainty and market stress to take advantage of market dislocations like we are seeing now, history has shown that doing so can be a meaningful source of wealth creation as investors seek to reach their long-term investment goals in the years ahead.

As we consider the impact of the dramatic weakening of consumer sentiment in Q1, the possibility of widespread global tariff implementation by the US, increased probability of a US recession, the breathtaking drawdown in US equity markets, fixed income yield and price volatility, we believe the term that best captures the current market tone is shaken. Confidence appears to be leaking, if not racing out, of almost every asset class, at a pace harkening back to the darkest days of COVID. We are reminded, in this moment, of the importance of disciplined and diversified asset allocation, together with a steadfast commitment to one’s long-term investment horizon. Deviation from these essential tenets can be disastrous in terms of achieving one’s investment objectives over time. For example, investors entered Q1 with the highest exposure to equities and the lowest exposure to fixed income in over a decade, according to Morningstar1. With the benefit of hindsight, we now see that investor asset allocations were sub-optimally positioned for the current market environment, vigorous portfolio rebalancing may not have been systematically applied as equity values surged by roughly 50% over the past two years and roughly 90% in the past five years.

While investors should be comforted by the fact that high-grade fixed income has helped preserve principal for investors during Q1, that may be little consolation for those with large exposures to high beta instruments. Municipal bond investors have also not been immune to recent market volatility. The flight to quality in the Treasury market, together with significant seasonal, tax-time selling by retail investors, seeking to make tax payments by April 15, has caused municipal bonds to underperform Treasuries year-to-date. For example, amidst the chaotic market gyrations just yesterday, April 7th, Treasury yields rose by roughly 30 basis points (bps), from intraday lows, yet municipal bond yields rose by 35 bps. Tax-free muni yields, on longer duration bonds, are now approaching 100% of the yield on taxable US Treasuries. Given that munis are tax-exempt and Treasury bonds are taxable, the 100% ratio has typically represented a very attractive entry point for investors as the tax-exemption is clearly being undervalued, in our view. Moreover, the absolute level of tax-free munis in the 20-30 year area of the curve is now approaching 5.00%, or a taxable equivalent yield of almost 10.00% for someone in the highest tax bracket. The selloff in munis, is due in part to investor fears that the tax-exemption of munis is at risk of revocation by Congress, to help pay for the extension of the Tax Cuts and Jobs Act. At CIM, we consider that outcome as an extremely low probability event, given the estimated revenue created would be roughly $250 billion over the next 10 years, while the higher borrowing costs that state and local governments would incur is estimated to exceed $800 billion. In addition, a recent National Law Review article clearly lays out that retroactively removing the tax-exemption of munis would likely violate the Federalist underpinnings of the 10th Amendment, thereby making the removal of the tax-exemption unconstitutional at face value. However, Congress does have the authority to restrict the issuance of tax-exempt bonds on a going forward basis. In the event Congress chose to remove the tax-exemption of all future muni bond issuance, doing so would dramatically increase the value of outstanding tax-free bonds, in our view. As we consider the underlying credit quality of the municipal issuers we hold on behalf of clients, we are reminded that very little has changed in the past few days, weeks, or months that would jeopardize the stable outlook for municipal credit quality more broadly.

The main question we have been fielding from many investors of late is very straight forward. What should we do now? If one’s investment horizon remains long-term in nature, we recommend revisiting your asset allocations to be sure your current portfolio properly represents your risk tolerance, consistent with your long-term goals. If you are properly allocated there is likely nothing one must do. While it is often easier said than done, we encourage investors to remain calm when faced with the volume of current market noise we are experiencing. For investors who have been fortunate to accumulate cash, we recommend locking in higher yields, especially those available on municipal bonds, as we expect the muni market to normalize at lower yields in the weeks and months ahead. While it is often difficult in times of uncertainty and market stress to take advantage of market dislocations like we are seeing now, history has shown that doing so can be a meaningful source of wealth creation as investors seek to reach their long-term investment goals in the years ahead.

If you should have any questions regarding this commentary or where we are finding the best values today, please do not hesitate to reach out to us.

Kindest Regards,

Andrew Clinton

CEO

- 1Morningstar: How Far Out-of-Wack are Fund Investors’s Asset Allocations? $800 Billion, Give or Take ↩︎

Please remember that past performance may not be indicative of future results. Net-of-fee performance returns are calculated by deducting the actual Clinton Investment Management, LLC investment management fee from the gross returns. Performance returns include the reinvestment of income and capital gains. Actual results may differ from the composite results depending upon the size of the account, investment objectives, guidelines and restrictions, inception of the account and other factors. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available upon request.

The views and opinions expressed are not necessarily those of the distributing firm or any affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent your firm’s policies, procedures, rules, and guidelines.