If your municipal bond manager didn’t proactively harvest meaningful losses via tax loss swapping during the first half of 2025, you likely missed out on one of the best opportunities in the past three years to protect your broader asset allocation from capital gains taxes. For this reason, we are providing important information below that, going forward, we believe can help municipal bond investors maximize their total after-tax return.

- While many municipal bond managers and investors often wait until the end of the year to harvest losses, Clinton Investment Management (CIM), through our Tax Optimization Protocol (TOP), proactively harvests losses throughout the year, as opportunities present themselves. We do so as we are fully aware that technical fluctuations in the muni market, often tied to temporary factors, as was the case in 2025, create fleeting conditions requiring diligence and responsive action.

- The application of our TOP overlay strategy has delivered real and meaningfully positive benefits, as the strength of this strategy is that has historically reduced the tax burden our clients would have otherwise been forced to pay

- CIM’s Municipal Credit Opportunities and intermediate Municipal Market Duration strategies have generated absolute returns that are among the highest in the municipal bond SMA industry*, over the past three years, cumulatively.

- When we consider the additional tax alpha** delivered to our clients, our strategies are among the most cost effective on a net-of-fees and after-tax basis.

- We understand there may be other municipal bond managers that “claim” to provide ongoing tax loss harvesting. That said, we also know that what a manager says and what they do are unfortunately not always the same. This is particularly true for 2025. CIM reports the tax alpha we generate directly on our strategy fact sheets for all advisors and investors to see. Be wary of any municipal bond manager that claims to provide tax harvesting yet is unable or unwilling to publicly disclose the tax alpha they generate. We frequently find municipal bond managers using tax loss harvesting language as part of their marketing strategy. Less often is it a material part of their overall investment strategy and protocols.

- We encourage investors to reach out to their municipal bond manager to discuss the extent to which they harvested losses on their behalf during the first six months of 2025. If the response from the manager is slow, evasive, or underwhelming, you are likely working with the wrong manager.

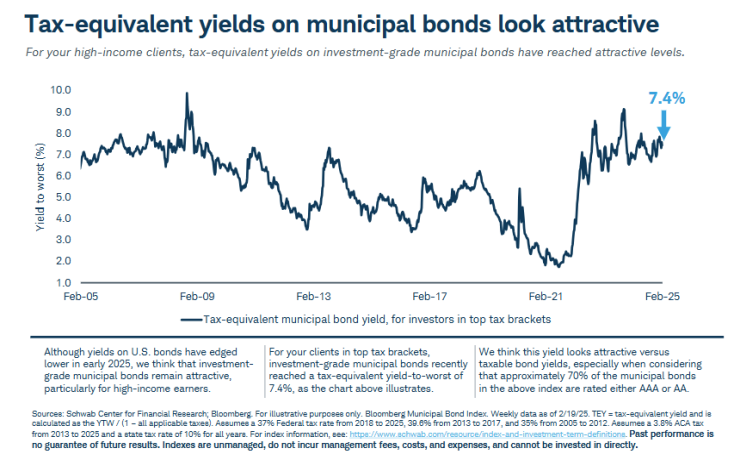

- Given this week’s news that continued cooling and moderation in inflation caused the Consumer Price Index (CPI) to come in below expectations, together with the Fed’s stated intention to lower interest rates further in 2026, investors are missing out on the rising “real” returns that municipal bonds, with maturities greater than ten years, currently offer.

- The muni yield curve is inverted between 1-4 years with yields of roughly 2.2%, while investors can achieve yields over 4.00% further out on the curve, equating to roughly 7%, on a taxable equivalent basis+ for those in the highest tax bracket. Munis continue to be one of the highest yielding fixed income solutions for investors seeking stable tax-free cash flow and enhanced portfolio diversification.

If you have any questions about our clearly differentiated municipal bond strategies and how our TOP overlay can help reduce your tax burden in the future, please feel free to reach out to us as we would be happy to assist in any way we can.

* PSN as of 9/30/2025

** CIM defines Tax Alpha as the potential value created through tax-loss harvesting techniques that fully offset a capital gain and is derived by calculating the composite capital losses divided by the average composite assets and multiplied by the maximum capital gains tax rate of 23.8% (20% plus 3.8% Net Investment Income Tax), for any stated period. Tax-loss harvesting is any transaction resulting in a capital loss. Although realized capital losses can potentially offset capital gains, reduce taxes paid, and enhance after-tax returns, individual results will vary dependent upon an investor’s actual tax rates, the presence of current or future capital loss carry forwards, and other investor specific tax circumstances. Tax-loss harvesting may not achieve actual value creation.

+ The taxable equivalent yield represents the yield that must be earned on a fully taxable investment in order to equal the tax-exempt yield of the composite. The taxable equivalent yield is calculated by dividing the tax-exempt yield by 1- the maximum federal income tax rate of 40.8% (37% federal + 3.8% NII tax).

This material has been provided for informational purposes only and is not intended by Clinton Investment Management to provide and should not be relied on for tax, legal or accounting advice. If such advice is required, please consult with your own tax, legal and accounting advisors.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure brochure discussing our advisory services and fees is available upon request.

The views and opinions expressed are not necessarily those of the distributing firm or any affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent your firm’s policies, procedures, rules, and guidelines.